The Plastic Philosophy: My Four-Card Contemplation

Part one of my series "Things I've Convinced Myself I Need." My ongoing series exploring the tools, systems, and small obsessions that shape daily life

Welcome to my FIRST installment in my examination of the mundane made meaningful.

This series delves into what I actually use day to day.

We’ll be exploring a few key areas of my life, with links to a lot of the products and methods ot how I use this. This will include: how I take care of myself (personal care), what helps me get work done as someone navigating ADHD (productivity tools), how I manage my mental health and Christian journey (faith and spirituality), my approach to physical health, and the systems I use to nurture relationships.

Today, we're contemplating credit cards, a brief meditation on the modern absurdity of optimizing financial instruments while pretending it's not just elaborate consumerism.

Obligatory transparency moment: The links below are referral links. If you click through and apply, I receive some form of compensation. Your terms remain unchanged, but my mortgage appreciates your consideration. We're all just trying to make it through capitalism together.

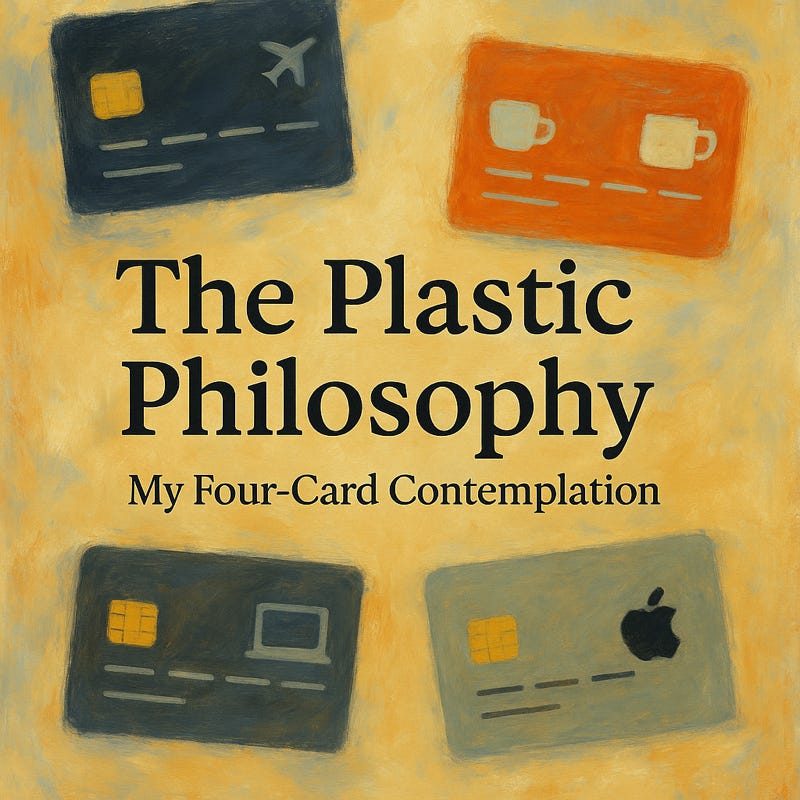

In my ongoing attempt to reconcile philosophical contemplation with practical living, I've arrived at what can only be described as a credit card strategy. Four pieces of plastic, each serving a distinct purpose in the theater of modern spending. Whether this represents optimization or elaborate self-deception remains an open question.

The Financial Foundation: Copilot Money

Before diving into the plastic, a word about the system that makes all this credit card choreography meaningful. My wife and I use Copilot Money to manage our household budget and finances (use referral code DRKRYW for 2 months free).

Without a clear view of our actual spending patterns and financial goals, credit card optimization becomes an elaborate form of financial theater. Copilot helps us understand where our money actually goes, which makes the strategic use of different cards feel less like an elaborate rationalization and more like an intentional choice.

The AMEX Platinum: An Exercise in Justified Excess

This card serves as my travel confessor, absorbing every flight, hotel, and rental car charge with the solemnity of expensive metal. The annual fee is obscene, naturally, but I've convinced myself it's justified through a careful dance of credit utilization:

Saks credits become holiday gifts (because nothing says "I love you" like a department store credit)

Digital subscription reimbursements cover NYTimes and Spotify (the modern utilities)

Walmart+ membership (suburban surrender, complete)

Resy Global Access for those date nights and necessary work meals

I strategically deployed this card for our new home appliances. This was a calculated move to hit the welcome bonus while furnishing our domestic monastery. The 5x points on travel feel almost generous until you remember they're essentially giving you back your own money, ever so slowly.

The Chase Sapphire Preferred: The Reliable Workhorse

My daily driver, this card handles the mundane reality of personal spending. While others chase category bonuses with spreadsheet precision, I've embraced the simplicity of one card for everything non-travel. Their point offerings create just enough value to feel smart without requiring a PhD in rewards optimization.

Sometimes the most profound choice is the boring one.

The Delta Reserve AMEX: The Art of Separation

Why two travel cards? Because work travel exists in its own moral universe, requiring its own financial container. Every work-related expense, flights, meals, hotels, and the inevitable airport coffee, goes here. This creates a clear separation between personal and professional spending, making expense reports less burdensome.

Combined with the Platinum, I've achieved what can only be described as lounge ubiquity. Whether this represents peak privilege or peak absurdity depends on your philosophical framework.

The Apple Card: Ecosystem Surrender

Used exclusively for Apple subscriptions and device purchases, this card represents my complete capitulation to the ecosystem. No rewards optimization here. Just a clean integration of paying Apple with Apple's own card. Sometimes surrender brings its own form of peace.

The Deeper Question

Four cards. Four purposes. Each represents a different aspect of how we've organized modern life around the movement of money. Whether this represents optimization or elaborate rationalization of consumer behavior remains delightfully unclear.

What's certain is that each card serves as a small boundary in the otherwise boundless flow of spending—creating just enough friction to force intentionality, even if that intention is simply "which piece of plastic do I use for this particular form of commerce?"

The Aaronists among you will recognize this as yet another example of finding philosophy in the mundane. The rest of you might just want the referral links.

Either way, we're all here contemplating the same questions: How do we move through a system designed to extract value while maintaining some semblance of intentionality? How do we optimize without losing our souls to optimization itself?

I don't have answers. I just have four carefully chosen pieces of plastic and the vague sense that I've thought about this more than is strictly necessary.

Questions for contemplation: What do your spending patterns reveal about your values? Is there such a thing as ethical consumption under capitalism? And why do we find comfort in organizing our financial chaos into neat categories?

Let me know in the comments which rabbit holes you've fallen down in the name of "optimization."